2023 Automotive Dealer Benchmarks Report

For the fifth consecutive year, Foureyes released its new automotive industry benchmarks. This data is intended to help dealers and dealer groups compare their performance against the industry and track trends in how leads behave – all in an effort to help you know what it takes to beat the competition and exceed your sales and marketing goals in 2023.

This year, Foureyes tracked, analyzed, and aggregated data from December 2021 - November 2022, which included more than:

- 700 million dealer website visits

- 11 million unique pieces of inventory

- 21,500 automotive dealership websites (including group sites)

To provide clear benchmarks, this report filters out website activity from bots, solicitors, job seekers, service customers, and other non-sales leads that dealers nationwide received.

Mishandled Leads

Dealers don’t want to leave prospects hanging out to dry, but it still happens. Overall, 37% of qualified leads were mishandled – that means leads with true buying intent weren’t logged to CRMs, had their calls missed, or experienced delayed follow-up. This metric has now improved year-over-year from each of the past two reports (41.6% in 2022, and 46.7% in 2021).

Hello??

Continuing to explore the types of “mishandled” leads, we found that 12.4% of qualified leads (i.e. again, have sales intent vs service calls or solicitors) were never logged to the dealer’s CRM – most of those (26.4%) stemming from website calls. This number is actually on the rise – in 2021, we saw 10.6% of leads going unlogged, and 11.7% in 2022. Low inventory is frequently the supposed answer for why this continues to increase – i.e. dealers knew they couldn’t help customers get what they wanted, and potentially were less incentivized to return phone calls or enter leads into their CRMs. While dealers may see a short term rise in their close rates (less leads in the overall bucket), they’re ultimately losing out on future deals when inventory inevitably returns.

Don’t you forget about me :(

This 66.2% statistic has held fairly constant over the last several years, according to Foureyes data. Dealers have dedicated resources into improving the sales process and customer experience, but aren’t necessarily seeing the fruits of their labor.

Lead Attribution

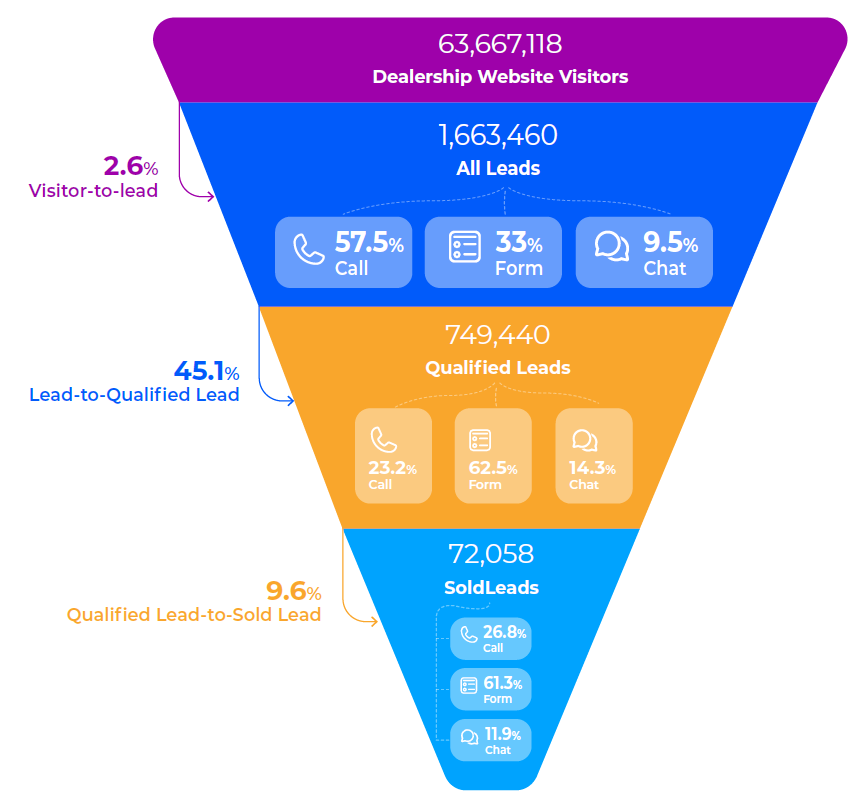

Here’s a funnel breakdown of more than 63 million dealership website visitors across the United States.

Calls via dealer websites generated the most “Leads,” however Forms accounted for the most “Qualified Leads” (i.e. those actually in the market to buy) and “Sold Leads."

A lot of dealers focus on conversion rates from visitor-to-lead. But we’re not seeing that number improve over time – it actually decreased from last year’s report (which analyzed much of 2021), where we saw a 2.8% conversion rate.

The number that probably matters to more dealers is “Lead-to-Qualified Lead.” Qualified leads are defined to filter out spam, bots, friends and family just calling to chat with staff, service leads, etc. How are your vendors filtering out those junk leads to really help your team get to the bottom of where your leads are coming from?

Days to Close

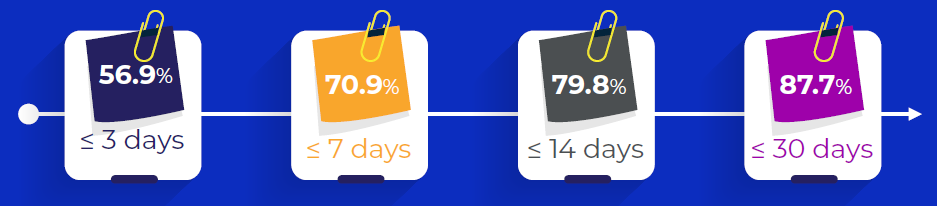

Among qualified leads that buy, 56.9%+ do so within three days of filling out a form, chat, or website call.

This is trending upwards in comparison to previous years, which is unsurprising when factoring in low inventory. People inquire about a specific vehicle, but ultimately find it unavailable and continue on their search.

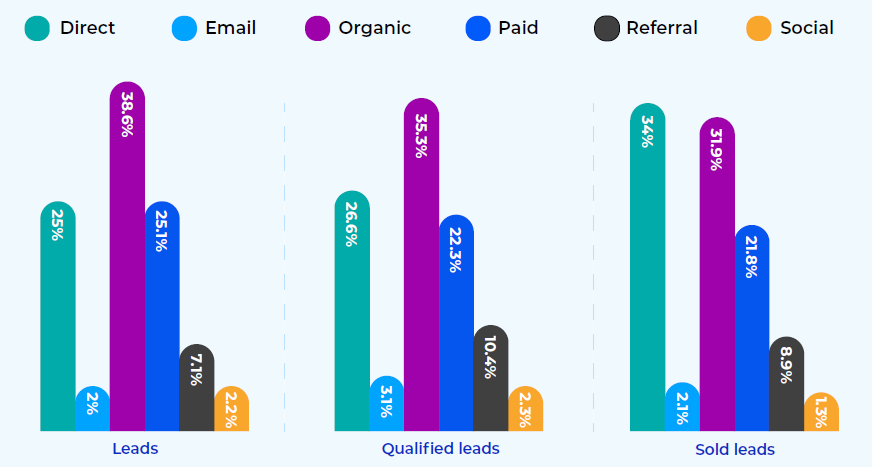

Leads by Channel

Which channels are dealers using to not just generate leads, but generate the right leads that will actually buy? (i.e. “Qualified” and “Sold” leads)

A higher percentage of Sold Leads (far right graph) came in with a “Direct” attribution, making it easy to see the value of personalized sales. Paid ads held steady across the three groups, indicating that customers are receptive to multiple touch points.

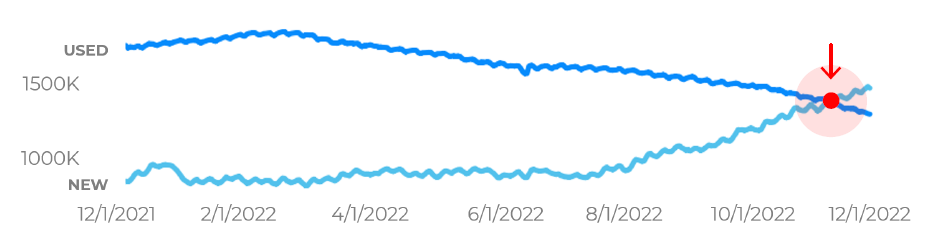

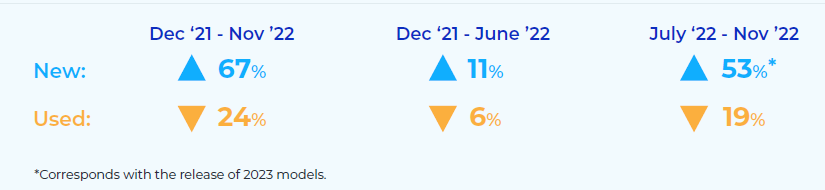

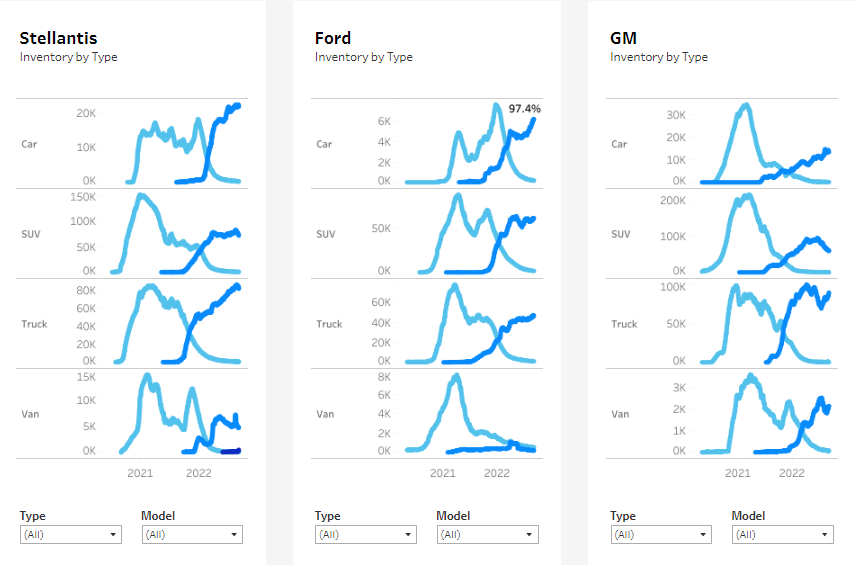

Inventory Volume Change

Notable last year, new inventory re-surpassed used inventory in November 2022 for the first time since April 2021.

While we are seeing inventory as a whole begin to rebound, that isn’t consistent for all dealers. Inventory continues to fluctuate depending on region, OEM, and even model.

The below table shows inventory percent change for the full 12 months, as well as the first and second halves of this reporting period. Notable in the second half of the year (July 2022 - November 2022) is the release of new 2023 model year inventory.

Price Listings

We often see domestic brands listing price more frequently than international or luxury brands. It’s helpful to note that those who don’t list price for any new inventory may also include sites requiring customers to submit more information to gain access to pricing information.

Inventory and Price Adjustments

This section is a snapshot of dealer activity in November 2022 – i.e. the most recent month of this report’s timeframe.

While this is just a snapshot of November 2022 data to demonstrate the most recent data from this reporting period, as a whole, we’re seeing a lot more price adjustments on used vehicles than new.

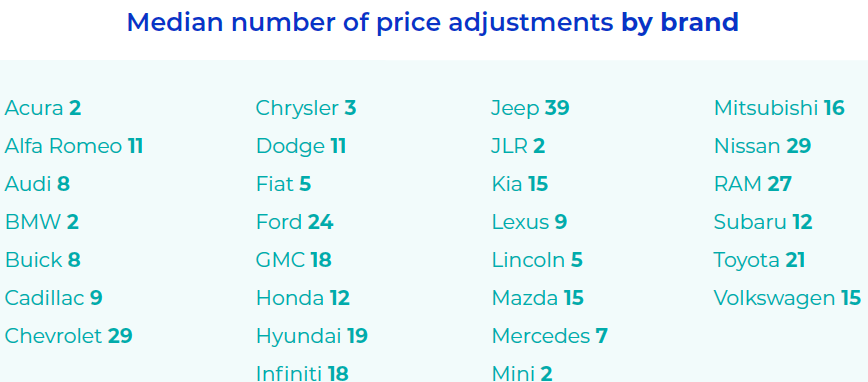

If we break it down further and look by OEM, we again see that domestic brands run a lot more incentives and price adjustments.

Beat These Benchmarks

Take advantage of these industry insights to keep a pulse on what’s happening in the market.

But you don’t have to do it alone. Foureyes quickly helps dealers and their groups close more of the leads they already have (in their CRMs, and from their website activity and inventory).

Connect with us to learn how!

Read More Blogs

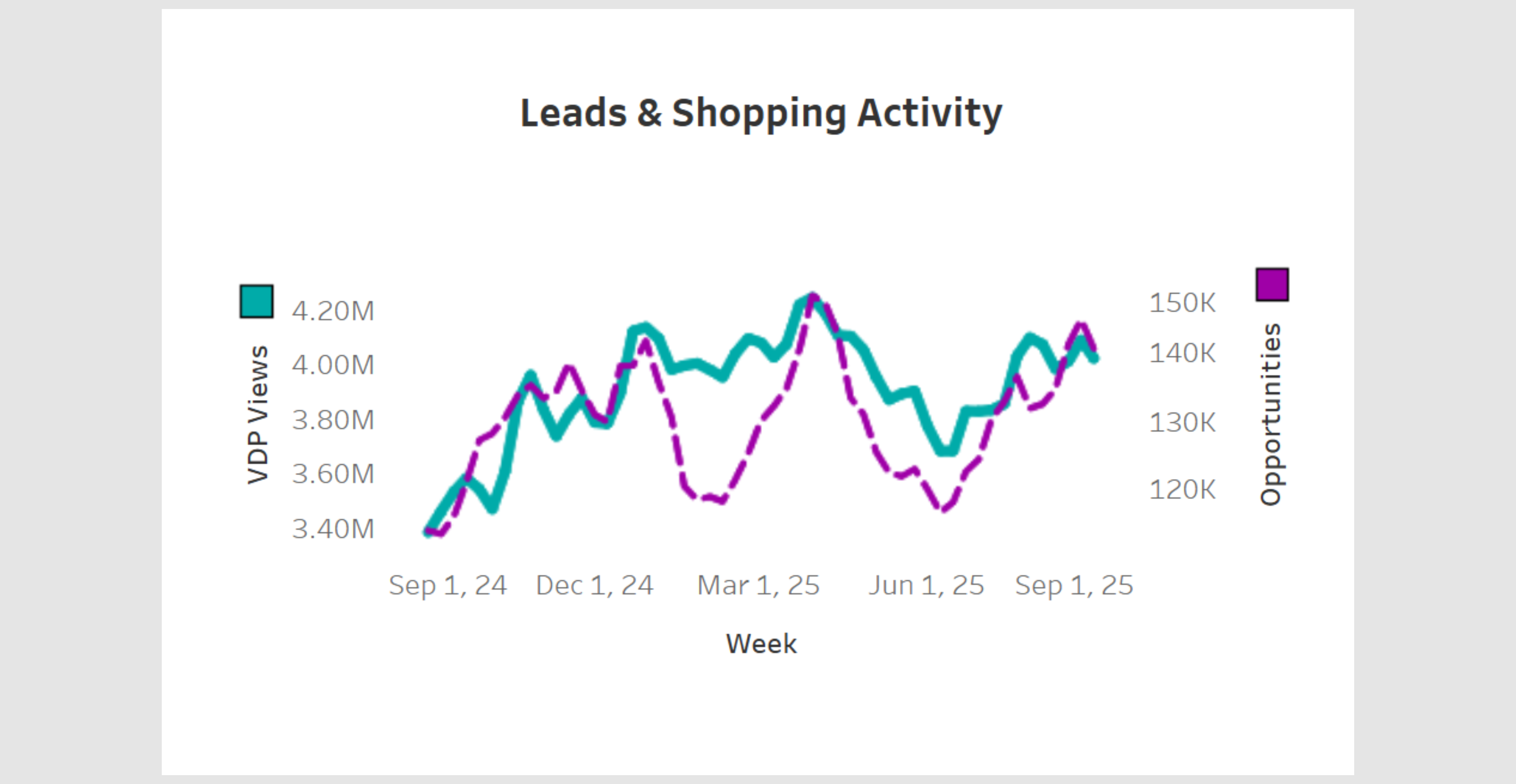

Data Study: How Many Leads Does it Take to Sell a Car in 2026?

Data Study: How Many Leads Does it Take to Sell a Car in 2026?The average new vehicle takes 3.3 leads to sell. EVs and performance models take far more, work trucks and mainstream crossovers far less.

Dealership Close Rates by Metro: And Why Contact Rates Matter

Dealership Close Rates by Metro: And Why Contact Rates MatterFoureyes tracked 2.6 million leads from more than 1,150 dealerships across 48 U.S. markets through Q1 2026 to dig deeper into dealership close rates by metropolitan area. One surprising finding: the correlation with contact rates.

2026 Automotive Dealer Benchmarks Report

2026 Automotive Dealer Benchmarks ReportFor the eighth year, Foureyes analyzed dealer website data to identify industry benchmarks, so you can compare your dealership’s performance and see what it takes to stay competitive.

Data Warehousing for Auto Dealerships: What It Is, Why It's Hard, and Why Your CDP Makes or Breaks It

Data Warehousing for Auto Dealerships: What It Is, Why It's Hard, and Why Your CDP Makes or Breaks ItData warehousing comes up constantly in dealer group conversations, but the actual mechanics rarely get explained clearly. This post tries to fix that. By the end you'll know what a warehouse actually does, why so many groups struggle to get it right, and why the data going in matters more than most people talk about.

Foureyes Launches Snowflake Managed Services, Taking the Complexity Out of Data Warehouse Management for Dealer Groups

Foureyes Launches Snowflake Managed Services, Taking the Complexity Out of Data Warehouse Management for Dealer GroupsNew offering gives dealer groups the warehousing expertise they need — without building and managing it themselves

.webp) Foureyes and Volie Announce New Integration Partnership to Boost BDC Performance

Foureyes and Volie Announce New Integration Partnership to Boost BDC PerformanceFoureyes and Volie announced a two-way integration partnership that connects audience-building and dealer data infrastructure with tools for dealership BDC teams.

New Foureyes Consent Management Passes 100-Vendor Milestone, Signaling Industry Standardization Around Dealer-Controlled Consent

New Foureyes Consent Management Passes 100-Vendor Milestone, Signaling Industry Standardization Around Dealer-Controlled ConsentFoureyes today announced that more than 100 automotive retail vendors are now participating in Foureyes Consent Management, marking a major step toward standardizing how customer communication opt-out requests are managed across the industry.

.png) Introducing Foureyes Connect: A New Standard for Automotive Data

Introducing Foureyes Connect: A New Standard for Automotive DataFoureyes today announced the launch of Foureyes Connect, a different kind of data platform designed to reset how dealer groups operate and scale in an increasingly complex automotive retail landscape.

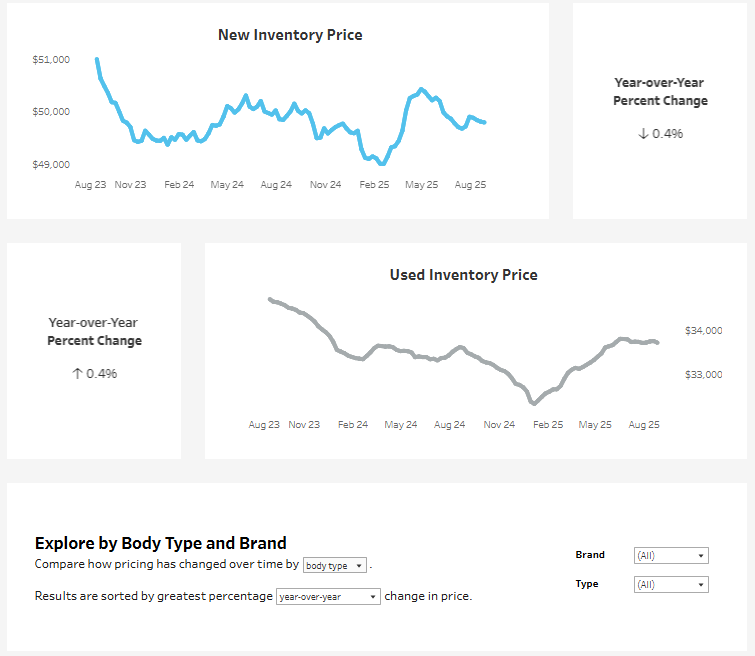

How to Use the U.S. Auto Prices Over Time Dashboard

How to Use the U.S. Auto Prices Over Time DashboardExplore weekly U.S. auto pricing trends with Foureyes’ interactive dashboard. Compare new and used prices by brand and body type, track inflation and tariff impacts, and uncover insights to guide smarter decisions.

How to Use the U.S. Automotive Inventory Over Time Dashboard

How to Use the U.S. Automotive Inventory Over Time DashboardTrack how U.S. auto inventory has changed since 2021 with this interactive dashboard. from Foureyes. Compare new vs. used, explore brand and model shifts, and gain insights to guide smarter pricing, stocking, and forecasting decisions on a weekly basis.

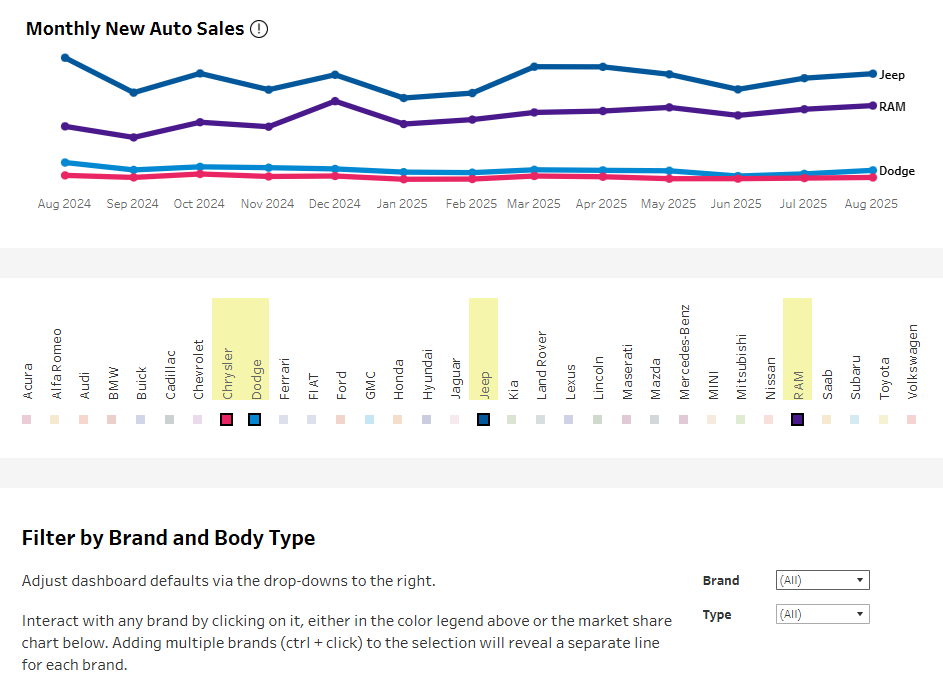

How to Use the U.S. Automotive New Vehicle Sales and Market Share Dashboard

How to Use the U.S. Automotive New Vehicle Sales and Market Share DashboardTrack monthly U.S. new vehicle sales and market share with this interactive dashboard from Foureyes. Compare brands, body types, and regions to uncover sales momentum, competitive shifts, and supply dynamics—updated monthly and available for free.

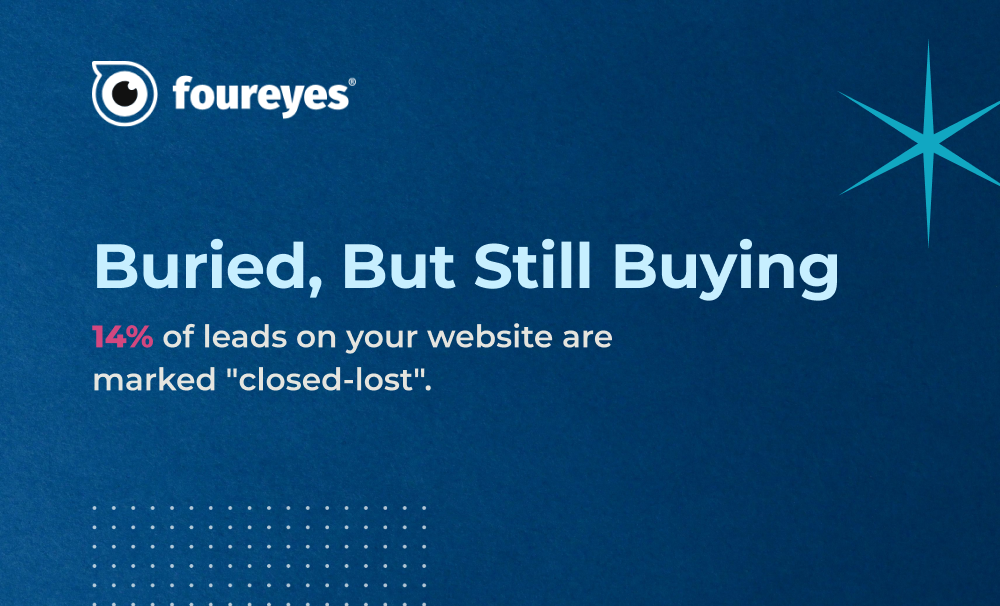

Data Study: The Leads You Marked as Lost Are Still Shopping

Data Study: The Leads You Marked as Lost Are Still ShoppingNew Foureyes data shows why “closed-lost” doesn’t mean game over – and how dealers can win more with what they already have.

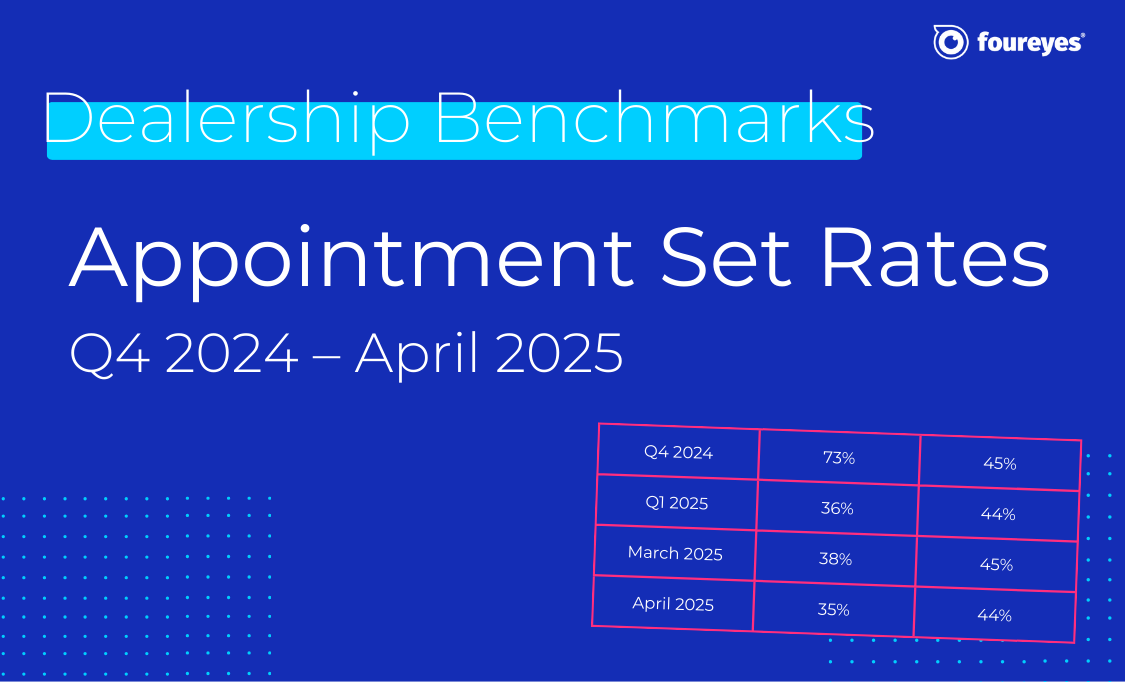

Automotive Sales Benchmarks: Appointment Set Rates for Q4 2024 to April 2025

Automotive Sales Benchmarks: Appointment Set Rates for Q4 2024 to April 2025If your dealership's appointment set rates feel like a mystery, you're not alone. But now, there's fresh data to show where you stand.

2025 Automotive Dealer Benchmarks Report

2025 Automotive Dealer Benchmarks ReportFor the seventh straight year, Foureyes has dropped its Automotive Dealer Benchmark Report – pulling back the curtain on what's really happening with your leads throughout your sales process.

Foureyes Changing the Follow-up Game with Inventory-based Texting

Foureyes Changing the Follow-up Game with Inventory-based TextingSee how the latest Foureyes innovation further helps dealerships match prospects to specific inventory.

There are How Many “Hidden” Sales Leads at Automotive Dealerships?

There are How Many “Hidden” Sales Leads at Automotive Dealerships?New research of sales process data across U.S. automotive dealerships sheds light on the opportunity of “hidden” leads in dealership CRMs.

How many leads do you actually need? And are you efficiently and effectively working them?

How many leads do you actually need? And are you efficiently and effectively working them?Which dials need to be turned, and how far, to ensure they are getting leads for inventory that actually need leads? And to ensure those leads efficiently and effectively worked?

How Many Leads Does it Take for Dealerships to Sell a Car?

How Many Leads Does it Take for Dealerships to Sell a Car?A Foureyes study of U.S. automotive dealerships identified the lead-to-sale “efficiency” across new vehicle inventory for Q1 2024.

2024 Automotive Dealer Benchmarks Report

2024 Automotive Dealer Benchmarks ReportFor the sixth consecutive year, Foureyes released its new automotive industry benchmarks. This data is intended to help dealers and dealer groups compare their performance against the industry and track trends in how leads behave.

.jpg)

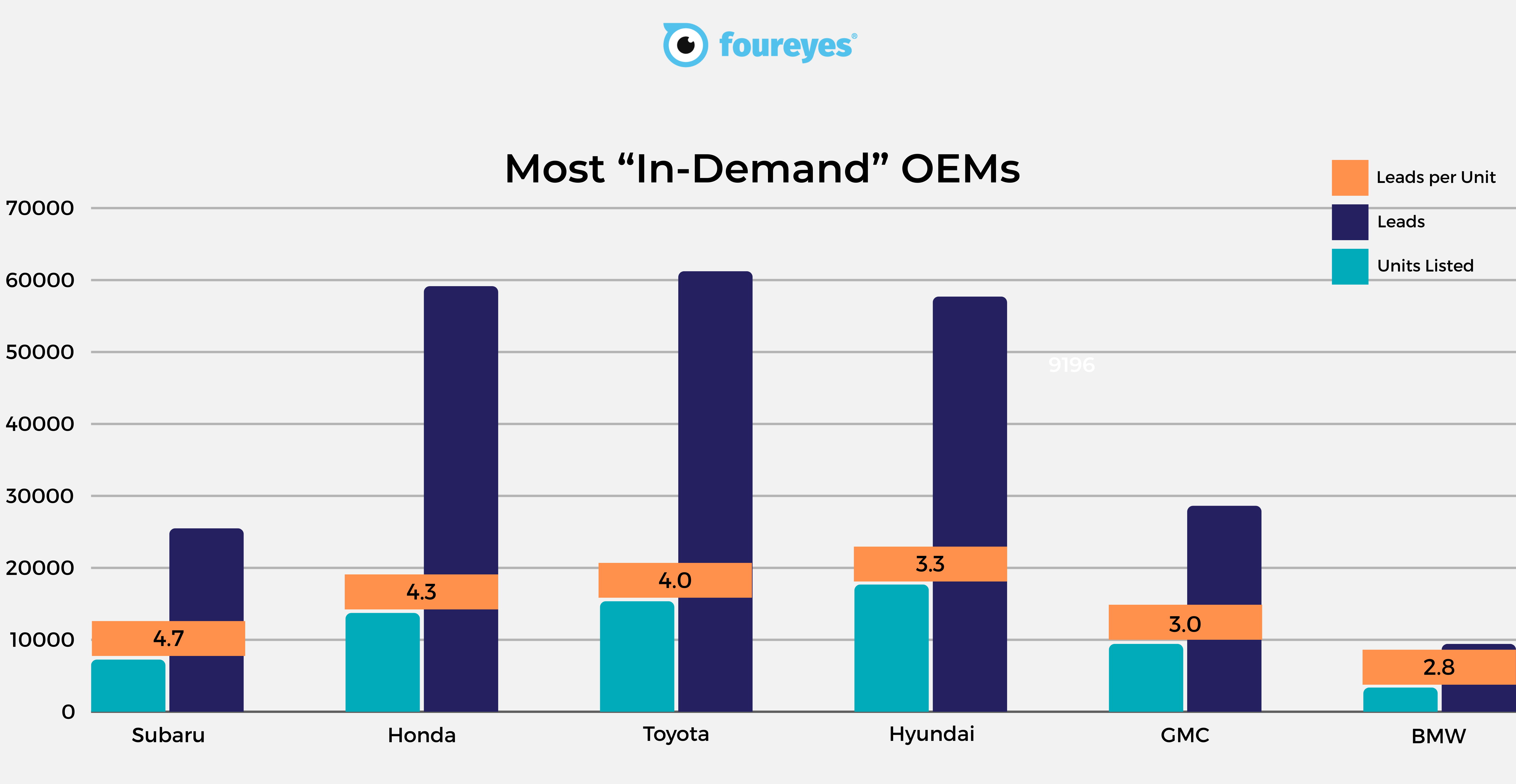

Most In-demand YMMs (2023 & 2024)

Most In-demand YMMs (2023 & 2024)We dove into a pool of approximately 700 dealerships to scope out the most sought-after 2023 and 2024 YMMs and their OEMs over the past 3 months (min. 100 units per YMM)

.png)

2022 Automotive Dealer Benchmarks Report

2022 Automotive Dealer Benchmarks ReportAs automotive dealerships continue to adjust their strategies, tactics, and other process operations during this ongoing vehicle inventory shortage, we at Foureyes are sharing – for the fourth consecutive year – new auto industry benchmarks intended to help dealers understand the market, track trends in how leads behave, and drive sales success in 2022.

2021 Automotive Dealer Benchmarks Report

2021 Automotive Dealer Benchmarks ReportFor the third year in a row, we’re sharing auto industry benchmarks to help dealers and OEMs understand the market, track changes in customer behavior, and drive sales success in 2021.

The 2020 Automotive Dealer Benchmarks Report

The 2020 Automotive Dealer Benchmarks ReportStart the new year off strong by reviewing your sales performance and creating 2020 goals. See how your dealership stacks up against the competition and use these auto industry benchmarks to develop a marketing and sales strategy for the new year.